.jpg)

Decentralised Finance (DeFi) is a movement and ideological approach to finance that seeks to recreate traditional financial systems in an open, transparent, and permissionless way, to give individuals direct control over their assets and financial interactions without relying on central authorities such as banks, governments, or other intermediaries.

The rise of Decentralised Finance, or DeFi, is more than a technological evolution; it is a philosophical statement about trust, control, and freedom in the realm of money. To understand DeFi, it is worth first reflecting on the centuries-long history of financial control and the limitations inherent in traditional finance.

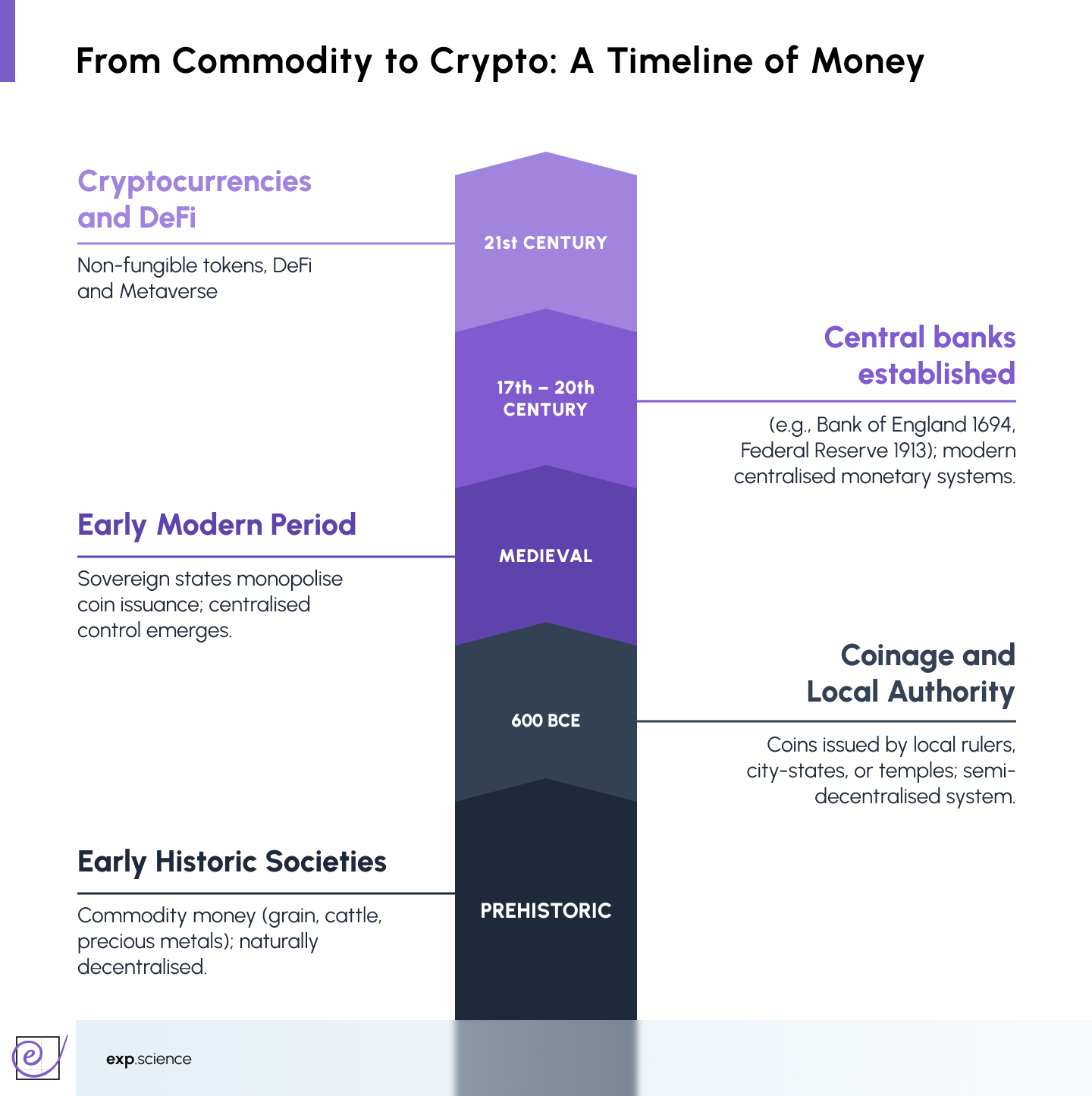

A Brief History of Financial Control and Regulation

Money was originally decentralised in nature. In prehistoric and early historic societies, it began as commodities with intrinsic value, such as grain, cattle, or precious metals, which anyone could use as a medium of exchange without relying on a central authority. Around 600 BCE, coins emerged in Lydia (modern Turkey) and spread across other regions.

Over time, as kingdoms and nations consolidated power, governments increasingly monopolised currency issuance. By the medieval and early modern periods, most coins were issued by sovereign states, which could control supply, standardise value, and enforce legal tender laws. This centralisation allowed governments to fund armies, collect taxes, and stabilise trade, but it limited competition and reduced personal control over money.

From the 17th to the 20th centuries, central banks such as the Bank of England (1694) and the Federal Reserve (1913) became the dominant issuers of money, solidifying a system in which nearly all national currencies are now centrally controlled and private issuance is heavily restricted or illegal. The emergence of central banking, fractional reserve banking, and national currencies codified the authority of central institutions.

Regulation evolved to protect markets and consumers, but often at the cost of flexibility and inclusivity and overarching control. DeFi challenges this paradigm by asking a radical question: can financial systems operate without centralised oversight while still maintaining trust?

Today, with the rise of cryptocurrencies and decentralised finance, there is a renewed interest in returning to a model in which individuals have direct control over their own money, echoing the original, decentralised nature of currency.

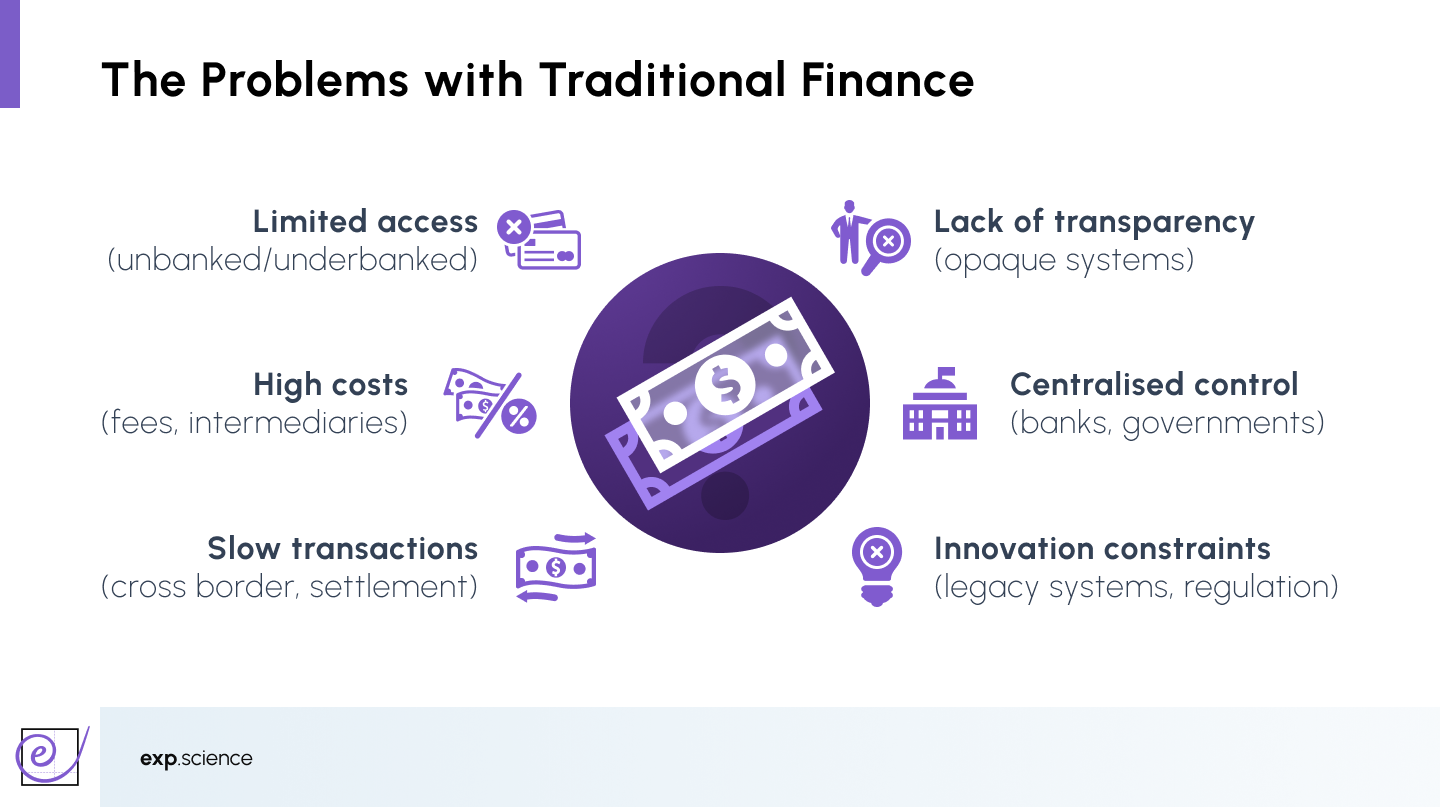

The Problems with Traditional Finance

For a significant portion of modern human history, financial systems have been tightly controlled by central authorities. Banks, governments, and regulatory bodies have acted as gatekeepers of economic activity, determining who can access credit, the growth of personal wealth, and which transactions are deemed legitimate. While these structures have provided stability and trust in large economies, they have also introduced profound inequities.

Traditional finance, or TradFi, is inherently hierarchical. Decisions are concentrated in the hands of a few. Access to financial services is often restricted by geography, socio-economic status, or political power. Furthermore, intermediaries extract value through fees and commissions, and opaque practices can obscure systemic risks.

The 2007-2008 global financial crisis starkly illustrated these vulnerabilities when centralised power, lack of transparency, and misaligned incentives culminated in catastrophic consequences for millions of people who had no influence over the institutions controlling their wealth. The crisis, triggered by the collapse of the US housing market and major institutions like Lehman Brothers, demonstrated the fragility of interconnected financial systems built on opacity and excessive risk-taking.

In the UK, Northern Rock's collapse required emergency taxpayer guarantees to prevent systemic failure, whilst the subsequent Eurozone debt crisis saw Greece bailed out through loans that primarily protected riskier international lenders rather than addressing the underlying economic hardships faced by Greek citizens. This apparent asymmetry of risk and reward, where profits were privatised but losses were socialised, led many to question the fundamental fairness of existing financial architecture.

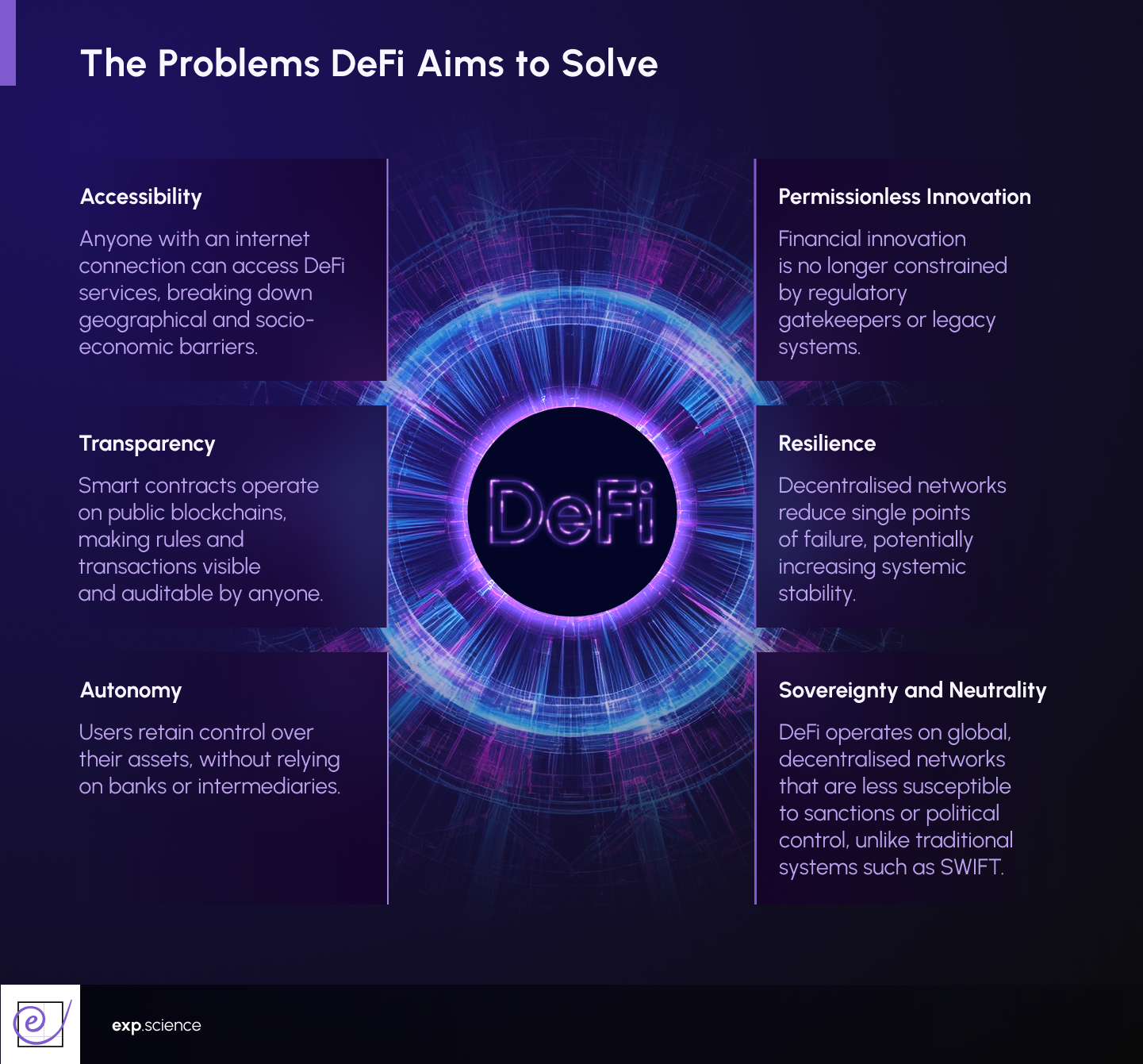

How DeFi Offers a Fair Alternative

Traditional financial systems have often perpetuated discrimination and bias by denying mortgages and loans to individuals based on race, gender, or other non-financial attributes, even when applicants possess identical credit profiles and qualifications. Structural and personal biases embedded in banking practices create barriers to financial inclusion, as human decision-makers have historically influenced outcomes in ways that disadvantage minorities and women.

Beyond individual discrimination, entire populations face exclusion through geopolitical sanctions enforced via systems like SWIFT, which can deny financial services to ordinary citizens of sanctioned countries who bear no responsibility for their governments' actions, effectively weaponising finance as a political tool.

In stark contrast, DeFi operates through autonomous smart contracts that evaluate objective data such as collateral, payment history, and transaction validity, without visibility into personal characteristics, nationality, or political considerations, and without human intervention.

By removing the subjective judgements of banking officials and the political constraints of centralised payment systems, DeFi creates a transparent system where decisions are governed solely by code, paving the way for fair, unbiased access to financial services regardless of one's background or country of origin.

The Emergence of DeFi

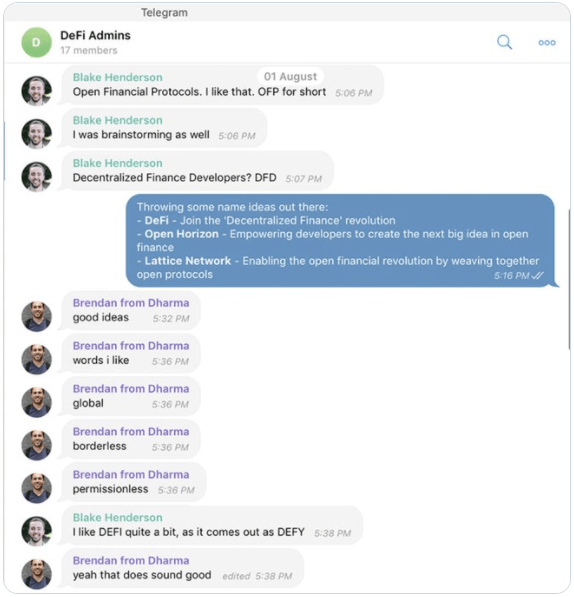

The term ‘Decentralised Finance,’ later shortened to DeFi, was coined in August 2018 during a Telegram chat between Ethereum developers and entrepreneurs, including Inje Yeo of Set Protocol, Blake Henderson of 0x and Brendan Forster of Dharma. Previously, the concept had been referred to as ‘open finance’ but had not been formally branded until this pivotal conversation.

These visionaries weren't just building applications, they were architecting an entirely new financial system where loans, exchanges, and savings accounts could operate in complete transparency, governed by code rather than corporate boardrooms. Their audacious goal: to democratise finance itself by making it open, permissionless, and accessible to anyone with an internet connection.

Yet the technological foundations for this financial revolution had been building for decades, beginning with Nick Szabo's prescient concept of smart contracts in the 1990s. These self-executing digital agreements that operate without human intervention lay dormant for decades until blockchain technology finally provided the infrastructure to bring his vision to life.

The early blockchain pioneers took tentative steps toward programmable money through platforms like NXT, Counterparty, and BitShares, but these experiments remained limited in scope and adoption.

The breakthrough came in 2015 when Ethereum launched as the first widely adopted general-purpose smart contract platform, providing the robust infrastructure needed to support complex financial applications at scale.. This transformed blockchain from a simple payment system into a programmable foundation capable of hosting complex financial applications. With Ethereum's arrival, the stage was finally set for the DeFi revolution that would follow.

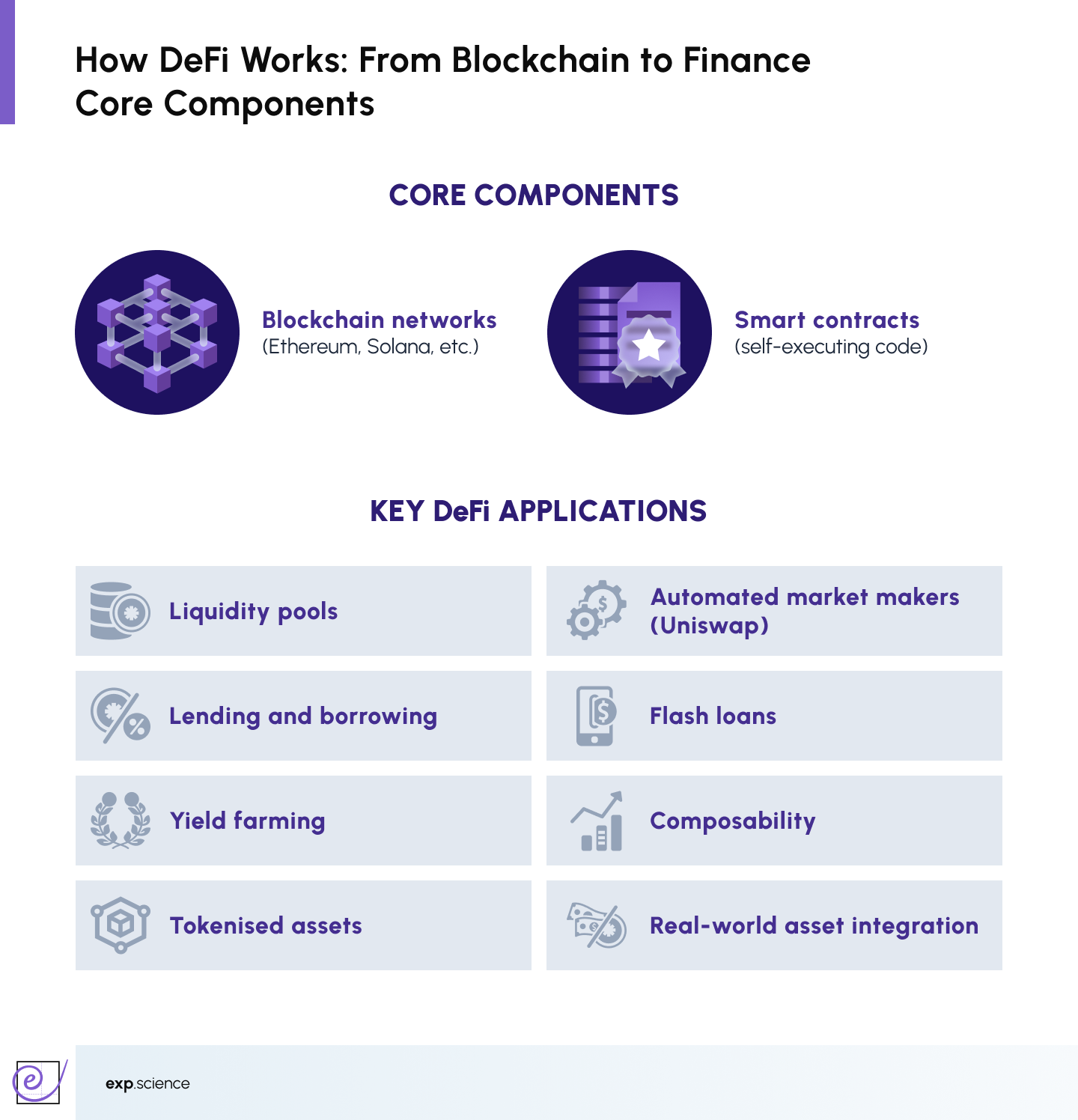

How DeFi Actually Works

At its core, DeFi operates through smart contracts, self-executing programmes stored on blockchain networks that automatically enforce agreements without human intervention. These digital contracts function like sophisticated vending machines: users deposit assets according to predetermined rules, and the contract automatically executes the agreed-upon transaction once conditions are met.

Several blockchains serve as infrastructure for DeFi applications, including Ethereum, Hedera, Solana, Avalanche, and others. These networks act as decentralised computers that process smart contracts. Unlike traditional banking systems that rely on human intermediaries to facilitate transactions, DeFi protocols operate through code that is publicly auditable and immutable once deployed.

Central to DeFi's functionality are liquidity pools, collections of cryptocurrency funds locked in smart contracts that provide the assets needed for various financial services. Rather than matching individual buyers and sellers like traditional exchanges, automated market makers (AMMs) such as SaucerSwap use mathematical algorithms to determine asset prices based on the ratio of tokens in these pools. When users trade, they interact directly with the pool, with prices adjusting automatically based on supply and demand.

Yield farming represents another fundamental mechanism, allowing users to earn rewards by providing liquidity to these pools or by lending their assets to borrowers through protocols like HeliSwap or Aave. Users essentially become the bank, earning interest from borrowers whilst the smart contract handles all the intermediary functions, from calculating interest rates to managing collateral and executing liquidations when necessary.

This automated system creates what developers term ‘composability,’ the ability to combine different DeFi protocols like building blocks. Users can simultaneously lend assets on one platform, use those lending receipts as collateral on another, and stake the borrowed funds elsewhere, creating complex financial strategies that would require multiple institutions and weeks of paperwork in traditional finance.

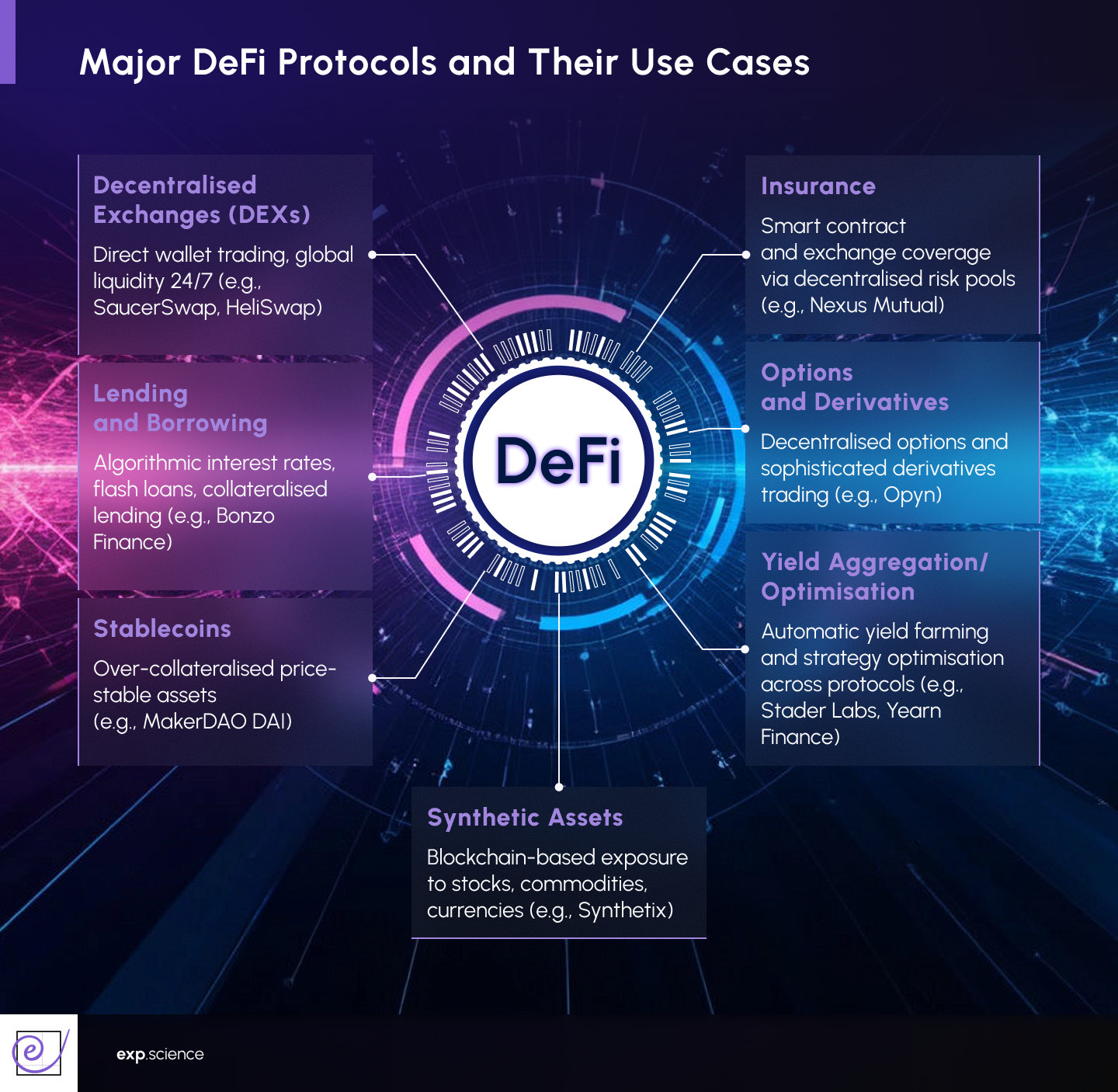

Major DeFi Protocols and Use Cases

The DeFi ecosystem has evolved into distinct categories, each addressing different aspects of traditional finance through decentralised protocols. Decentralised exchanges (DEXs) like Uniswap, SushiSwap, and Curve have fundamentally transformed how assets are traded by eliminating the need for centralised order books. These platforms enable users to trade directly from their wallets, maintaining custody of their funds throughout the process whilst accessing global liquidity 24/7.

Lending and borrowing protocols represent the most mature segment of DeFi. Compound pioneered the concept of algorithmic interest rates that adjust automatically based on supply and demand, whilst Aave introduced innovations like flash loans. These uncollateralised loans must be borrowed and repaid within a single transaction. These protocols have processed billions in lending volume, demonstrating that algorithmic credit markets can function effectively without traditional credit assessments.

MakerDAO's DAI stablecoin system showcases DeFi's approach to creating price-stable assets through over-collateralisation rather than traditional banking reserves. Users lock up volatile cryptocurrencies as collateral to mint DAI, which maintains its dollar peg through a sophisticated system of incentives and automated liquidations. This creates a decentralised alternative to centralised stablecoins like USDC or Tether.

Synthetic asset protocols such as Synthetix enable users to gain exposure to traditional financial instruments, from commodities to foreign currencies to stock indices, without leaving the blockchain ecosystem. These protocols use a combination of collateralisation and oracle price feeds to create synthetic versions of real-world assets that track their underlying prices.

Insurance protocols like Nexus Mutual provide coverage against smart contract failures, exchange hacks, and other DeFi-specific risks through decentralised risk pools. Members contribute funds and collectively decide on claims, creating a mutual insurance model that operates entirely through smart contracts and governance tokens.

More recent innovations include options protocols like Opyn, which enable sophisticated derivatives trading, and aggregators like Yearn Finance that automatically optimise users' yield farming strategies across multiple protocols. These demonstrate DeFi's rapid evolution from simple lending and trading to complex financial instruments that rival traditional finance in sophistication.

Risks and Challenges

Despite its revolutionary potential, DeFi faces significant technical, economic, and operational risks. The sector has seen billions of dollars drained through various exploits and attacks, with smart contract vulnerabilities representing one of the most fundamental challenges, where bugs in code can lead to permanent loss of funds.

Unlike traditional banking errors that can often be reversed, blockchain transactions are designed to be immutable and irreversible. Only once in blockchain history has a major hack been reversed, the 2016 DAO exploit on Ethereum, which required an unprecedented and highly controversial hard fork that permanently split the community and created Ethereum Classic. This exceptional intervention demonstrates both the theoretical possibility and practical impossibility of reversing blockchain transactions, making code security absolutely paramount.

The principle of ‘code is law’ creates a double-edged sword: whilst it eliminates human manipulation and bias, it also means that programming errors become immutable financial law. Impermanent loss presents a subtler but significant risk for liquidity providers, who face potential losses when token price ratios change compared to simply holding assets, a mathematical reality that can make providing liquidity less profitable than basic holding strategies during volatile conditions.

Regulatory uncertainty looms large over the entire ecosystem, as governments struggle to apply existing financial regulations to systems operating without central intermediaries..

Governance risks emerge from token-based voting systems where large holders can control protocol changes, potentially creating oligarchic structures. Additionally, many protocols retain administrative keys allowing unilateral developer changes, representing centralisation risks that could be exploited by malicious actors or compelled by authorities.

Current State and Adoption

The DeFi sector has achieved remarkable growth since its inception, demonstrating confidence in decentralised financial systems, suggesting that DeFi has established itself as a permanent fixture in the global financial landscape. The user base has evolved significantly from the early days of yield farming speculation. Institutional adoption has accelerated, with traditional financial firms increasingly integrating DeFi protocols into their treasury management and trading operations. This institutional participation has brought greater liquidity and stability to many protocols, though it has also raised questions about whether DeFi is fulfilling its original promise of financial democratisation.

Geographic adoption patterns reveal DeFi's global reach, with significant usage in regions where traditional banking infrastructure is limited or where currency devaluation creates demand for alternative financial systems. Countries experiencing hyperinflation or banking instability have seen particularly strong DeFi adoption, validating the technology's utility for financial inclusion.

DeFi stands at a crossroads, facing an existential tension between its decentralised ethos and the centralising forces of regulatory control. More than financial tools, DeFi represents a philosophical statement about trust, power, and freedom, making current regulatory pressure a fundamental contest over the future of financial power itself.

Governments worldwide grapple with systems operating beyond their traditional authority, creating inevitable friction between regulators seeking centralised oversight and protocols' commitment to decentralisation. The CFTC's 2025 CLARITY Act exemplifies attempts to fit decentralised systems into existing frameworks, whilst developers adapt through hybrid governance models to preserve independence whilst navigating compliance demands.

Technological advances in scalability and accessibility promise to democratise DeFi for billions, yet each involves trade-offs that could determine whether DeFi maintains its revolutionary character or succumbs to centralised control. Institutional integration brings liquidity but risks recreating the hierarchical structures DeFi sought to dismantle, whilst environmental pressures accelerate shifts to energy-efficient systems.

Ultimately, DeFi's survival depends on resisting the gravitational pull of centralisation whilst evolving to meet legitimate needs. This delicate balance will determine whether this experiment in decentralised finance fulfils its promise of restoring human agency or becomes absorbed into the traditional system it once sought to replace.

.jpg)

.jpg)

.jpg)